Areas of intervention by SAI Latvia during COVID-19

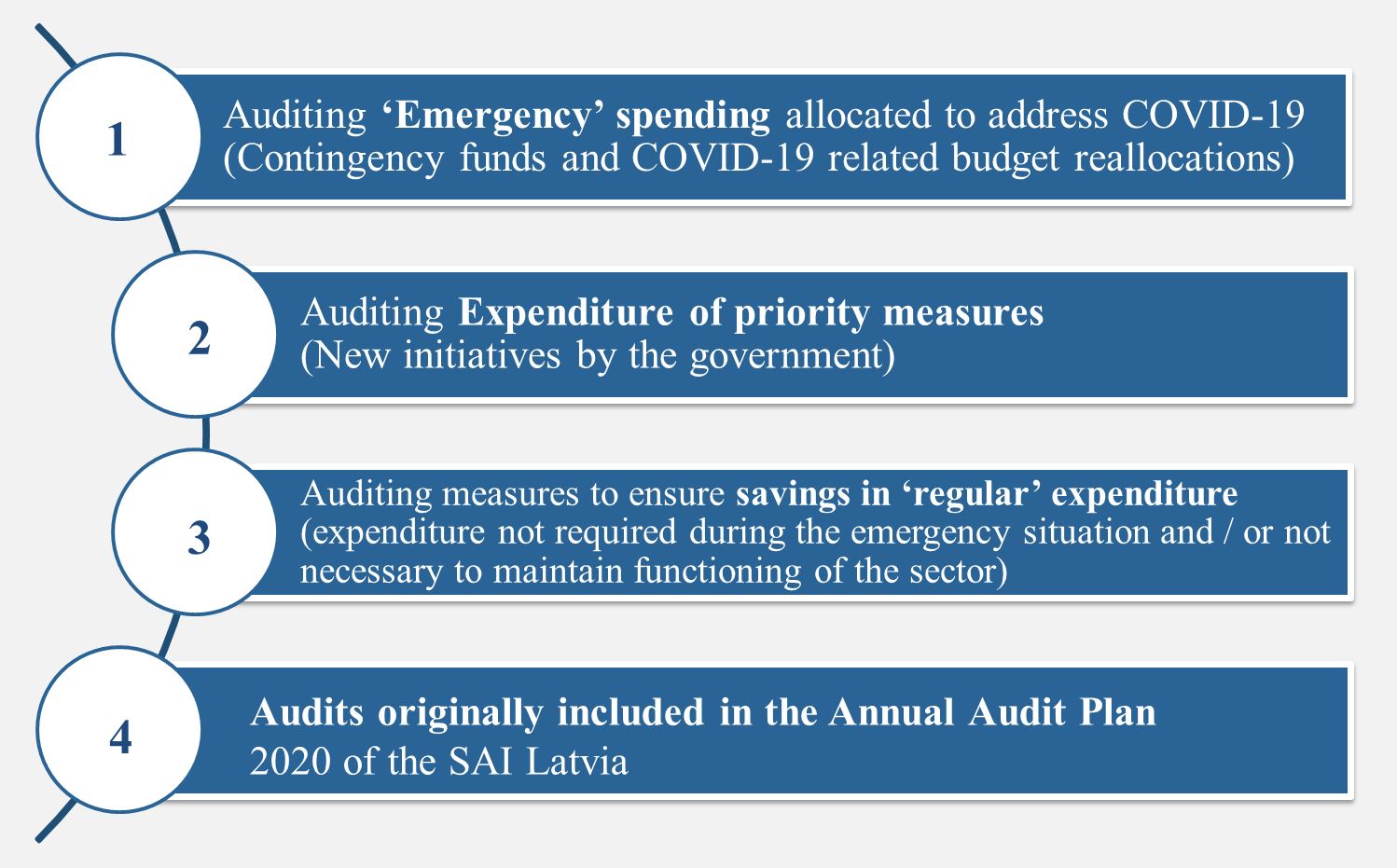

Area of intervention 1: Auditing ‘Emergency’ spending allocated to address COVID-19 (Contingency funds and COVID-19 related budget reallocations).

We shall assess a number of aspects, such as, whether:

- the objectives and results to be achieved with the emergency funds are clearly defined and the funding has been used according to the intended objective;

- there is no tendency to make full use of all funding without assessing its actual need for achieving the objective;

- there is an appropriate internal control system established environment to ensure that the appropriation reaches the intended beneficiaries;

- public procurements have followed the principle of ‘efficiency’?

We shall obtain evidences in ministries and central state institutions, state-owned enterprises and municipal enterprises, associations and foundations. We shall communicate audit results immediately after the measures funded by emergency funding are completed, taking into account the resources of the State Audit Office.

Area of intervention 2: Auditing Expenditure of priority measures (New initiatives by the government).

We shall assess whether the 2020 state budget funds allocated for the implementation of priority development measures have been used in compliance with legal requirements, in line with the intended objective, and have ensured the expected results.

For each priority measure examined, we shall provide a separate compliance opinion; we shall publish the results upon completion of our financial audits for 2020, i.e. May 2021.

Area of intervention 3: Auditing measures to ensure savings in ‘regular’ expenditure (expenditure not required during the emergency situation and / or not necessary to maintain functioning of the sector).

We shall assess whether there were financial appropriations for public institutions in the 2020 budget which were not required during the emergency situation and thus could be re-allocated to the budget programme “Contingency funds” in order to, at least partly, compensate for the increase in budget deficit.

We shall assess four budget categories: remuneration, services, goods and fixed capital. We shall publish audit results in April 2021, however, we plan to inform the Ministry of Finance on interim results regarding the first half-year spending already in September 2020.

Area of intervention 4: Audits originally included in the Annual Audit Plan 2020 of the SAI Latvia.

SAI Latvia has postponed launching a number of compliance, performance and combined audits, which were originally included in the Annual Audit Plan 2020 due to re-allocation of resources to auditing government’s COVID-19 response measures.

However, a number of originally planned audits have been launched, are on-going and will be finalized by the original deadlines.