Back

The State Audit Office publishes the audit “How does Alūksne Regional Government work? ”, which assesses whether the regional government has acted lawfully and expediently with financial resources and property, performing its autonomous functions. The audit has concluded that the decisions and actions taken by the regional government were not always founded on the population needs-based targets and were not always traceable and transparent. This is evidenced by the long-term operation without the basic documents of medium-term development planning and the implementation of projects that were not included in them.

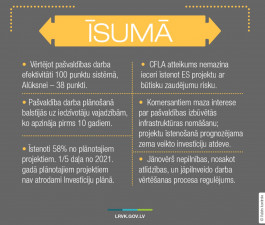

BRIEFLY

- When assessing the performance of the regional government as per score system of 100, Alūksne scored 38.

- The regional government based its work planning on the needs of the population identified 10 years ago.

- There are 58% of planned projects implemented. 1/5 of the projects planned for 2021 cannot be found in the Investment Plan.

- The refusal of the Central Finance and Contracting Agency does not detract from the intention to implement an EU project with a significant risk of loss.

- Economic operators have little interest in renting the infrastructure built by the regional government; low return on investment is expected in the implementation of projects.

- Weaknesses in setting remuneration must be addressed and the regulation of the performance evaluation process must be improved.